A Unique, Tried and Tested Route to Obtaining Sound Retrocession Pricing Control

The Practical Objective:

The practical objective is to provide clients with a clear competitive advantage through meaningful cost control when shopping for their retrocession protections.

The Dilemma:

Often, retrocession buyers find it difficult to assess the relative value of their programmes. When assessed against clients’ in-house modelled expected loss projections, variations in pricing can range from as low as twice the expected loss value to as much as eight times for the same coverage: this is despite that coverage being sourced from only a limited number of sellers through an even smaller number of specialist brokers.

Ceded reinsurance spend is a very important part of the capital management process, due to the current historically high levels of costs and retentions that have followed poor loss experience in property classes during the last decade, notably 2004, 2005 and 2008. Retrocession represents the most extreme example of aggressive pricing by the small number of remaining markets. But why should some buyers pay significantly more than others?

Where does your programme stand in relation to those of your peers and competitors?

The Explanation:

It is relatively easy for insurers to compare the cost of their reinsurance programmes to the price for their assumed exposures, given the development of proprietary modelling and capital management tools: indeed, many buyers and sellers use the same tools, as do their brokers. The process is made easier if exposures are homogeneous in terms of types of risk, perils, and limited territory covered, which frequently they are.

Retrocession programmes are different, since exposures are often multi-peril and multi-territory. Currently, the big three modelling companies offer no retrocession modelling and pricing tools on the open market, principally due to the difficulty of overcoming the opacity of underlying exposures to reinsurance accounts.

However; PG Butler’s unique proprietary exposure analysis and pricing techniques have created an index against which clients can benchmark their programmes relative to those of the market as a whole. The index is backed by over thirty years experience in the retrocession market and the collection and analysis of data from thousands of contracts over that period. These techniques and analysis form the basis of PG Butler’s successful retrocession underwriting and were assessed in depth by Standard & Poor’s whilst rating the “Puma” transaction.

The Conclusion:

By accessing this unique index, clients will establish an intelligent, informed base from which to make cost effective decisions regarding retrocession structures and pricing.

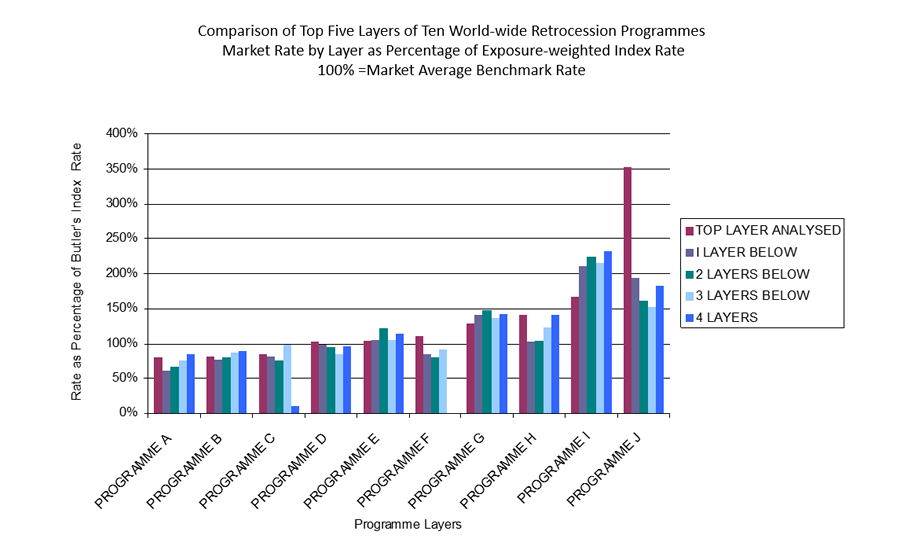

The specimen chart below illustrates the real price variations for the top four layers of ten programmes: such layers are more commonly exposure rated than the low-level, or “working”, layers. The “Market Benchmark Average Rate” is the percentage rate that the entire market pays for each $1 of exposure ceded to their programmes, based on PG Butler’s analysis.: 100% equals the average paid by all buyers from all markets.